Paper gold, paper bitcoin: Is there a problem with ETFs?

When Satoshi Nakamoto published Bitcoin in 2009, the innovation introduced a radically new form of transparency into the global financial world. Every transaction, every coin, each block can be viewed and checked in real time. No other investment class has offered such an open general book.

This was a clear break with traditional systems such as gold, in which the actual circulation can only be estimated and depends on intermediate dealers. But today new questions arise: Are we experiencing the rise of “paper bitcoin”-a synthetic version of the wealth value that threatens the transparency on which Bitcoin was built up?

Paper gold: the analogy

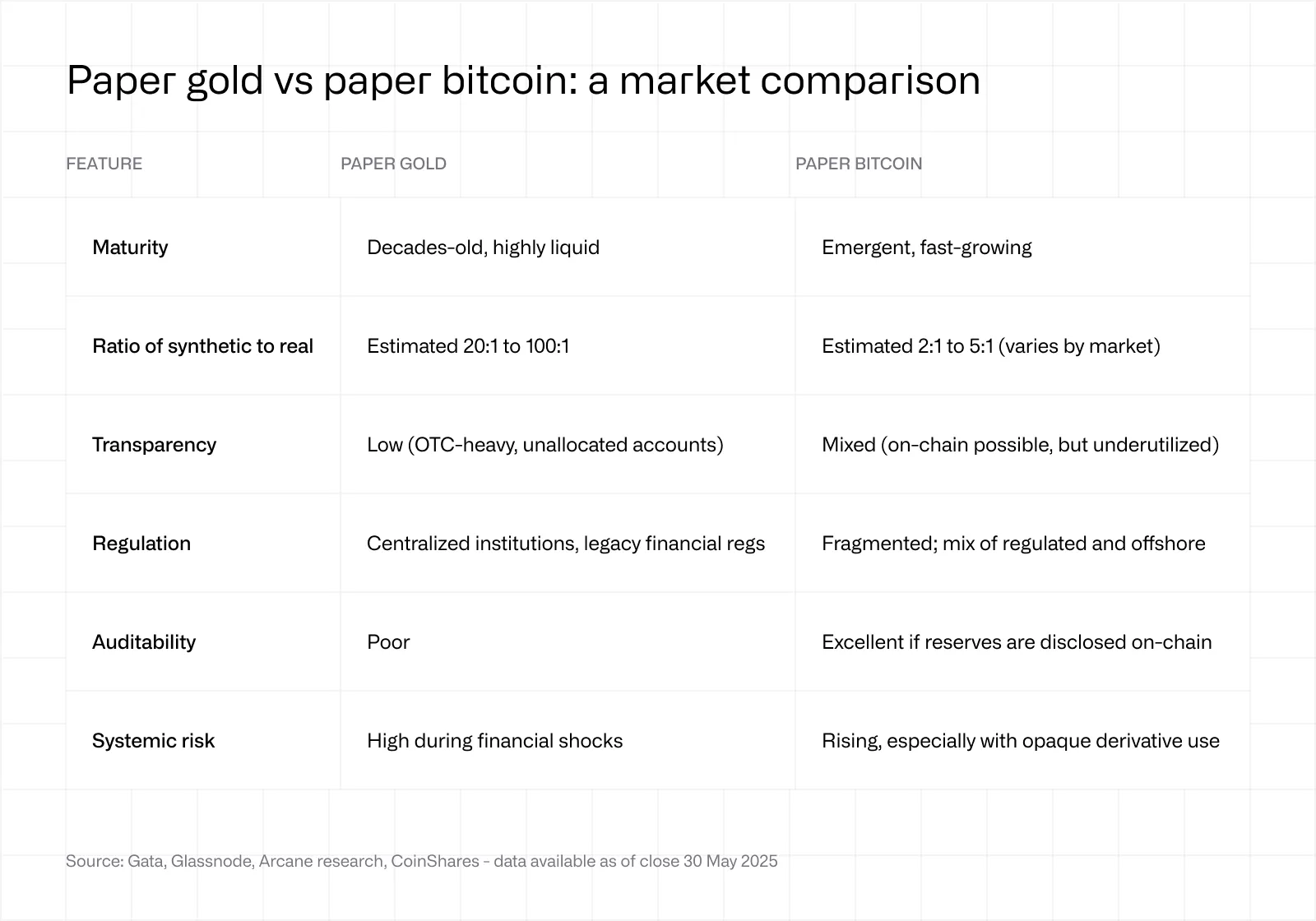

To understand this problem, we have to look at the history of the “paper gold”. Originally introduced with special educational rights in the 1960s, the term today describes financial products that offer a commitment to gold without physical gold being kept. This includes ETFs, appointment contracts and stocks of gold mines. Even if they are comfortable and liquid, these instruments bring counterparty risks with them and disguise how much physical gold they actually cover.

Over time, the majority of the gold trade shifted into opaque over-the-counter markets, especially to London. According to the World Gold Council, over 70% of the gold -large trading transactions take place out of the market, with limited public transparency. And in contrast to Bitcoins fixed limit of 21 million, the total amount of gold – including the occurrence in the ground – is speculative.

Paper bitcoin: The growing concern

Bitcoin, often referred to as “digital gold”, increasingly takes over similar financial structures: futures, options, ETFs and custody models. Although these instruments enable wider access, investors can also decouple from the underlying asset – especially if issuers do not ensure complete transparency.

The term “paper bitcoin” gained in importance than in September 2024 Announced allegations. Coinbase, storage of several Bitcoin ETFs, including Blackrocks Ishares Bitcoin Trust, is said to have said to have spent guilt notes instead of keeping real bitcoins. Although Coinbase CEO Brian Armstrong rejected these claims and Adam Back publicly refuted them, the incident caused unrest across the sector.

The assumption of “paper bitcoin” spread on social networks, often based on the perception that it was unusual if the Bitcoin course remains in a narrow price range despite the growing number of treasury companies and rapid ETF growth. According to this view, increasing institutional engagement should lead directly to a stronger upward movement.

However, this assumption is incorrect, since bitcoins is subject to complex mechanisms: price development is not determined exclusively by ETF inflows or balance sheet allocations. Factors such as market depth, derivative positioning, macroeconomic sentiment, the behavior of the miners and the activity of long -term owners also play a role. In addition, not all ETF inflows lead directly to purchases on the spot market: some issuers secure themselves with futures or use internal market-making structures, which means that the expected price effect can water.

Understanding Bitcoins market structure therefore requires a look beyond the headlines- at the interaction of spot, derivative and storage markets.

Nevertheless: If “paper bitcoin” spreads without solid verification, a return to a state in which market participants can no longer be sure to be sure whether the assets are actually 1: 1-a contradiction to bitcoins founding ethos.

Proof of reserve: tool or illusion?

After Intachination of FTX in 2022 the industry for Proof of Reserve (POR) was committed as a protective measure. Ideally, POR confirms that a company has the assets that indicate it ideally in relation to its liabilities. But Proof of Reserve can also be a facade, as reserves can be bloated temporarily before audits and there are no uniform standards for their publication. One example is crypto exchanges: If users cannot check the deposits of a stock exchange in real time via their deposit address, partial reserves could be a reality. Delayed payments are also a warning signal.

In the case of listed Bitcoin treasury companies, one could note that- Metaplanet except – None of them currently offers a way to review their stocks independently.

However, it is important to emphasize that issuers of publicly traded products and funds are subject to the provisions of the traditional financial system and must meet the reporting requirements of the respective stock exchange spaces.

The contradiction of Adam Back

When the rumor wave came up in September 2024, Bitcoin pioneer Adam Back reacted immediately and made it clear that there was no evidence that coin base had issued uncovered bliss. Be Comment Remembered: Skepticism should be based on data, not nourished by social media. The incident nevertheless emphasized a central knowledge: perception is just as crucial for market trust as facts.

At the same time, all rumors circulating on the Internet and on social media should be considered carefully. In 2024, Bloomberg-ETF analyst emphasized Eric Balchunas expresslythat in his 20-year industry experience there was never a case in which the underlying asset was not with the storage.

In addition, it is important to understand that the disclosure of stocks is more complex than simply displaying a public address-especially because this address is exposed to spam attacks such as “Dusting”, in which attackers send small amounts of assets to an address without consent. Such assets can be considered “contaminated”, for example.

But Bitcoin offers something that no other asset can: complete transparency. However, this promise is at risk if financial engineering overtakes the verification. Investors should ask for more than just convenience: they should demand cryptographic certainty.

The threat from “paper bitcoin” is real-but avoidable. By accounting for institutions, promoting best practices and consistently using the possibilities of blockchain, we can ensure that Bitcoin remains what it should always be: without trust, verifiable and radically transparent.

{kind=link}