Michael Saylor: When does Strategy become a systemic risk of Bitcoin?

The company Microstrategy, founded by businessman Michael Saylor in 1989, is now simply called Strategy – but either one thing has not changed under this new brand name: the massive acquisition of Bitcoin in the name of the company.

Its new logo is already adorned with that Bitcoin-Symbol, which unequivocally underlines the founder's strong commitment to the crypto asset. In this report, we explain in this report what this strategy has been used again and how it can be evaluated from a risk analysis perspective.

The strategy behind the Bitcoin purchases

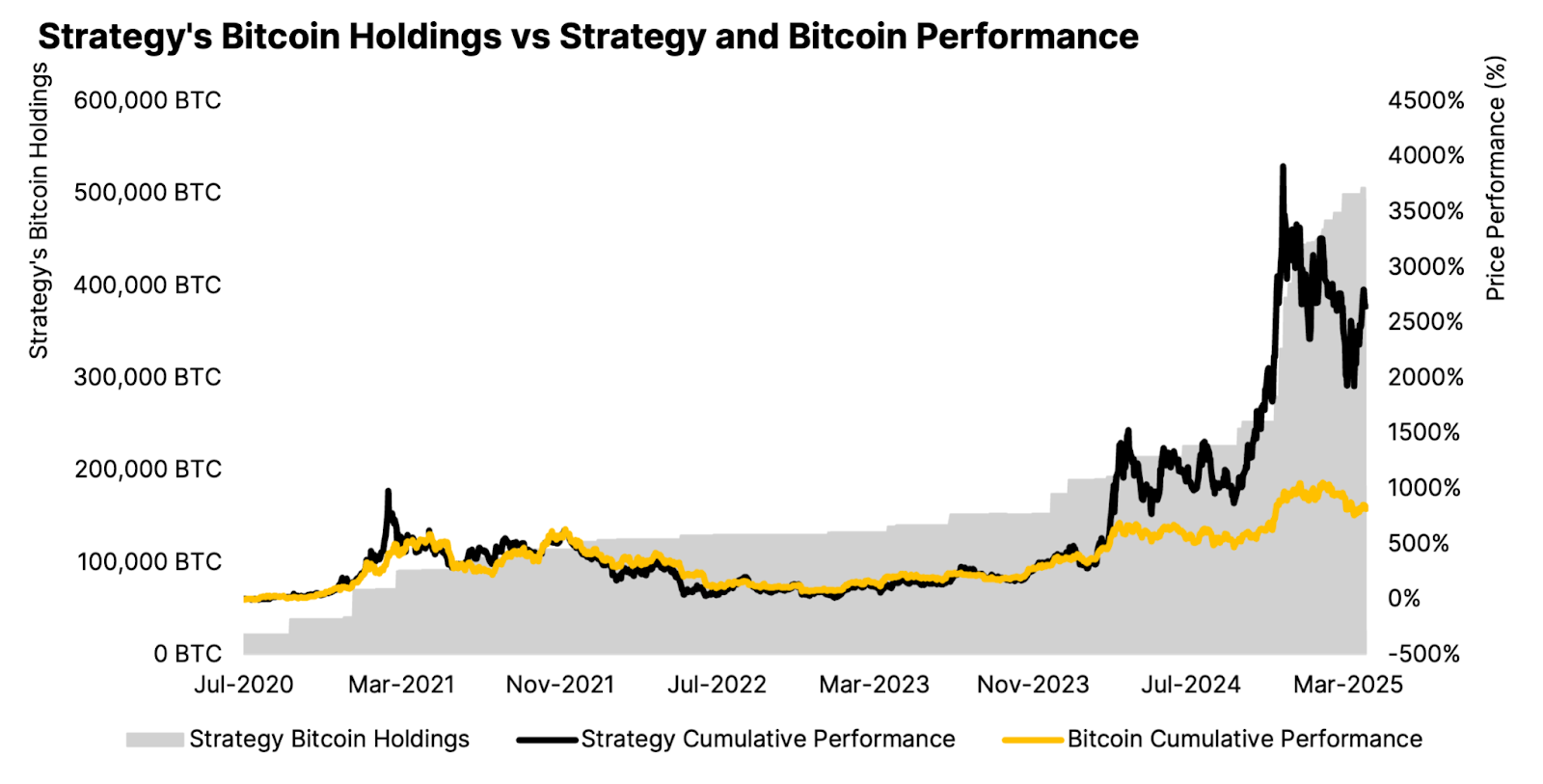

Strategy pursues a unique approach by buying large amounts of Bitcoin and For this purpose, a mixture of own and debt capital uses. The company currently has 528,185 BTC-this already corresponds to about 2.5 percent (!) Of the maximum available Bitcoin offer. With a total value of approximately $ 43 billion at a Bitcoin course of $ 81,000, Strategy is by far the largest company holder from Bitcoin.

It is particularly noteworthy that Strategy not only uses its own capital, but also takes on debt to further expand its Bitcoin position. A significant part of the financing takes place via so -called “convertible notes”, ie changeable bonds. These financing instruments offer investors the opportunity to convert their bonds under certain conditions in corporate shares instead of demanding a classic repayment in the form of cash. This reduces the immediate pressure on strategy to repay the debt of operational income or Bitcoin sales.

In addition to the changeable bonds, Strategy also finances his Bitcoin purchases through preferred shares and classic debts. As part of the so-called “21/21-Plan”, the company plans to procure another $ 42 billion in 2025 to 2027-of which 21 billion in the form of equity and fixed-interest financing instruments-primarily for buying further Bitcoin. Part of it are eternal preferred shares with a kupon of 10 percent that are specifically marketed to private investors.

The big question for investors: How risky is Saylor's strategy?

On the one hand, the use of convertible bonds for buying gives the company a high level of flexibility. Since these are not covered directly by Bitcoin, there is no immediate risk of liquidation if the Bitcoin price breaks. In addition, Strategy is not only a pure Bitcoin buyer, but still has a profitable software division, which implements around $ 463 million annually. This contributes to stability because it can cover the interest and dividend obligations of around $ 228 million a year.

At the same time, Strategy with his strategy is of course strongly dependent on the Bitcoin course. If there is a massive drop in price, the company could be forced to sell parts of its stocks to operate liabilities. However, a complete liquidation to repay all debts would require the fall of the Bitcoin price to approx. $ 20,143-a drastic decline compared to the current prices, which is not excluded.

For comparison: In the summer of 2024, sales waves of several large institutions provided considerable price pressure on Bitcoin. As both the Crypto belts Mt. Gox and Genesis as well as the German federal government Bitcoin worth $ 16 billion sold, he lost over 11 percent of its value in just one month. The story also shows that Bitcoin has always recovered from such shocks. So if Strategy is forced to sell larger quantities, this could exert pressure at short notice, but could not trigger a sustainable market crisis.

Conclusion: a bold but not unreasonable bet

With its aggressive Bitcoin purchases, Strategy relies on a long-term upgrading of the asset and also reflects the interests of more and more states and central banks, Bitcoin in anticipation of a long-term rise strategic reserve to keep. As a participant in a so -called “reserve race”, the company relies on innovative financing channels that reduce the risk of liquidation. Nevertheless, the model is not without dangers: a drastic Bitcoin price drop could increase the debt burden and put pressure on the value of the company.

For investors, this means a risky but potentially extremely profitable bet: Anyone who believes in Bitcoin's long -term increase in value could see Strategy as one of the most important players in this area – with all the opportunities and risks that bring with it.

{kind=link}