RWA tokenization: real assets on the blockchain

Imagine that you have a piece of a luxury villa in Bali, a share of gold in a safe in Zurich or an engagement in US state bonds-all about a smartphone, in a few minutes, without a broker. That is the promise of RWA tokenization.

Once exclusively reserved for institutional giants and wealthy private individuals, assets such as real estate, bonds and raw materials are now converted into blockchain-based tokens-accessible worldwide, available around the clock and immediately liquidable.

- The tokenization of real assets (Real-World Assets, Rwas) converts tangible assets such as real estate, gold and government bonds into blockchain-native tokens-with integrated KYC, custody and compliance.

- Institutions such as Blackrock, JPmorgan and Visa are driving adoption-together with crypto-native protocols such as Ondo and Centrifuge.

- Ethereum, Solana and Avalanche offer the sophisticated infrastructure to scalable and securely emit token assets.

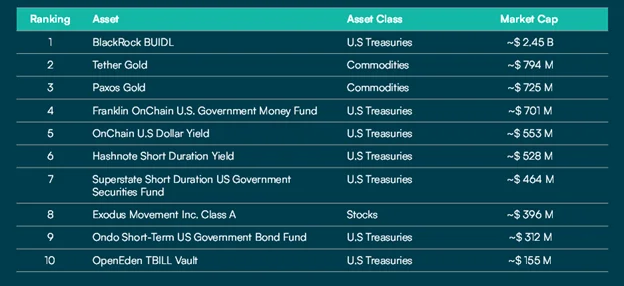

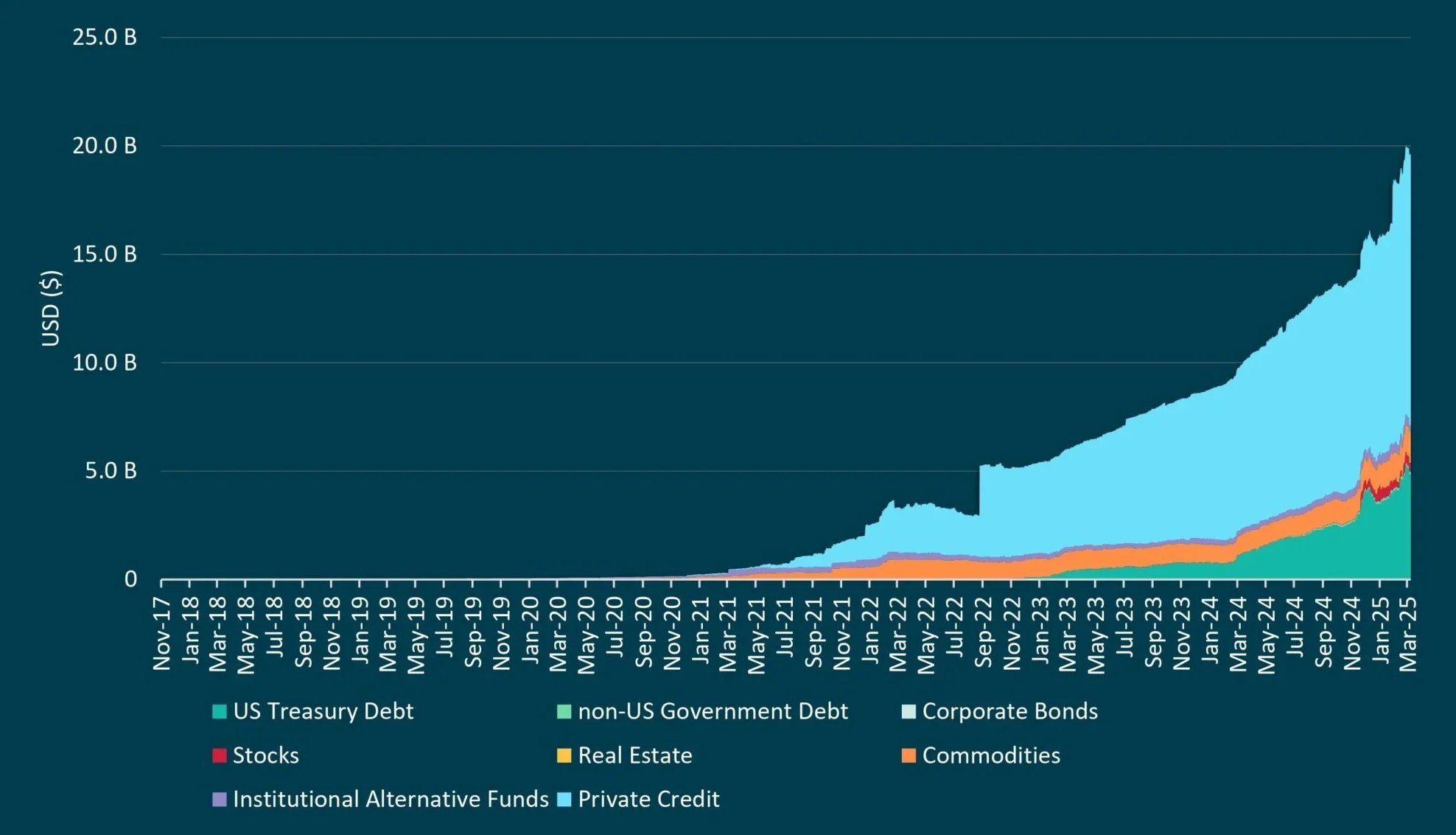

- RWA platforms currently manage over $ 10 billion in assets (without stable coins), with Blackrocks Buidl Fund at the top with around USD 1.95 billion.

- The RWA infrastructure matures thanks to progress in blockchain technology and enables deeper integration into defi.

- What's next? The markets are developing in the direction of tokenized ETFs, bonds and real collateral that can be used natively in defi ecosystems.

The rise of the Real World Assets (RWAS)

Real-World Assets (Rwas) quickly develop into a load-bearing pillar of the blockchain adoption and drive the convergence of traditional financial world and decentralized infrastructure. What was once a niche now seems to be at the center of global capital markets. Institutions like BlackRockHSBC and JPMorgan actively research blockchain infrastructures in order to token a wide range of assets-from US state bonds to private credit markets. Governments are also involved: the Hong Kong currency authority emitted tokenized green bonds on-chain; Singapore Project Guardian tests tokenized government bonds; And Grossbritannia's Management Office tested blockchain-based handling of government bonds.

Meanwhile, crypto-native platforms like Ondo Finance and Centrifuge forward the innovation. They develop specialized protocols that enable users to invest in tokenized guilt titles – essentially loans in digitized, transparent form – as well as in reigning assets that offer potential for interest interest – without traditional financial intermediaries.

But how did we get to this point – and where does this development lead? Let us examine the evolution of RWA tokenization, the underlying technology, the resulting regulatory framework and the transformative potential of this movement in the global financial system.

The beginning: early experiments (2015 to 2018)

The tokenization of RWAS began as a bold idea: What would be if physical assets could be displayed on the blockchain? Early pioneers like Digix brought gold -covered tokens on Ethereum. Projects such as Harbor and Polymath began to develop tokenized securities that acted as digital stocks of real companies.

In 2018, an apartment in Manhattan was token on Ethereum. Investors have now been able to invest proportionately in real estate on the blockchain – proof that tokenization was no longer theory.

The upswing: from real estate to bonds (2019 to 2020)

From 2019, platforms enabled the smallest parts of different assets – from real estate to invoices. At the same time, institutions began testing tokenized corporate bonds. The narrative changed from “What would be if?” To “What's next?”

With the rise of Defi in 2020, this change accelerated. Tokenized assets were now able to serve as collateral for loans, integrated into return strategies and traded around the clock. RWAs became active building blocks of decentralized ecosystems.

When the technology catches up (2021 to 2022)

Blockchain pioneers like Solana continued to drive the concept forward. Smart contracts automated ownership and distributions. Oracles like Chainlink delivered real -time prices. Institutional custody solutions strengthened trust. RWA tokenization changed from an idea to a resilient financial product.

How it works: convert real assets into tokens

The first step is to identify an asset – such as real estate, raw materials, credit portfolios or government bonds. Legal exams and ratings take place in advance. The asset is divided into individual digital tokens, each of which represents a share of ownership. These are shaped on blockchains such as Ethereum, Solana or others – depending on the speed, costs and regulatory requirements.

Compliance is required from the start. Investors have to go through KYC and AML tests. Licensed custody secures the assets. Smart contracts automate ownership, distributions and catering. After the emission, RWA tokens can be traded on centralized and decentralized platforms. Some are listed on regulated stock exchanges, others are integrated into Defi. Investors can achieve passive income through rental income, interest or defi returns.

The new market landscape: key players and emerging trends

Protocols and platforms drive the RWA revolution ahead in various areas. Ondo Finance runs a protocol to token US state bonds and brings fixed-income systems to the blockchain. Centrifuge transforms the market for private loans by securing loans and invoices with real assets. Maple Finance enables access to tokenized private loan in decentralized markets.

Blackrocks Buidl-Fonds, which tokens short-term government bonds on Ethereum, shows how serious some institutions mean by this area. The traditional financial world follows: Franklin Templeton and Wisdomtree have put on tokenized funds, JPMorgan tests on-chain conflicts and visas examines the integration of tokenized returns in payment systems. Real assets are now at the interface of Tradfi and Defi – with unprecedented liquidity, transparency and programmable property.

Regulatory obstacles and compliance hurdles

Despite progress, there are legal and regulatory challenges. Know your Customer (KYC) and anti-Money Lundering (AML) are mandatory in most legal areas. In the United States, the SEC and finces of platforms require compliance with identity tests. From December 2024, uniform regulation of digital assets will come into force. Singapore and the VAE are progressing with innovation -friendly but strict rules.

However, the classification of tokenized assets remains complex. In the United States, the Howey test is used, which means that RWAS often applies as securities. Switzerland follows a differentiated approach. The regulation remains fragmented-Europe is making progress with Mica, while Asia and the Middle East drive innovation-driven RWA initiatives.

DWAS comes next for tokenization?

The infrastructure for tokenization is – institutions are actively involved and regulation continues to develop steadily. In the coming years, trillions could be brought to real assets on-chain-tokenized government bonds, real estate and raw materials could become part of Defi. Improved interoperability will facilitate cross-border and chain transfer transfer.

Imagine a bond that is shaped on Ethereum and stored on Solana as security. A token for a property in Singapore, which is rehearsed under Swiss law. The legally and technological convergence could redefine the global financial system. On-chain identities and KYC standards will simplify compliance. Token ETFs and structured products could soon appear in everyday finance apps.

RWA tokenization is more than just a crypto application-it changes the way in which values are created, transferred and made accessible. By combining the flexibility of Defi to the trust of traditional financial systems, tokenized assets could become as common as ETFs or bonds. The same applies to private investors and institutions: The era of RWA tokenization is not even imminent-it has already started and only picks up speed.

{kind=link}